Why have a pension?

In this guest blog post wealth management consultant Matthew O’Hara from Mattioli Woods explains why it’s important to have a pension.

Millions of people in the UK do not save nearly enough to provide them with the standard of living they desire in retirement.

The state pension age is currently 66, however for those born after 5 April 1960 there will be a phased increase to 67, and eventually for those born after 5 April 1977 a phased increase to 68 (although the government has just announced a consultation which may lead to a review of this). With the full state pension currently at £179.60 a week (£9,339.20 a year) for the tax year 2021/22, this is far below what most people are likely to need to provide the level of income they hope to retire on.

According to a recent article in the Telegraph, after a lifetime of saving, the average UK pension pot stands at £61,8971, which with current annuity rates would buy you an average retirement income of around £3,000 per year from age 67. Add this to the full state pension and that makes just over £12,300 a year (£1,025 per month), which for many just is not going to be enough to maintain their lifestyle, meaning they may have to work later in life or lower expectations of what they will be able to afford in retirement.

But why save into a pension when you could just invest or save it yourself in a bank savings account?

Clients often tell me how complex they find pensions and one client even described them to me as a ‘dark art’. Pensions can be tricky to understand, but they really do not have to be. A pension is basically a long-term savings plan with tax relief, that grows throughout your working life to provide you with an income in retirement.

There are many types of defined contribution pensions, such as a personal pension plan, or a workplace scheme that you pay into via your employer, both which tend to be invested in a variety of assets, including stock market-based investments. Since the government introduced ‘automatic enrolment’ rules in 2012 employers now have to enrol all eligible job holders into a workplace pension scheme. You can of course opt-out however, unless the same contributions are diverted to a pension of your choice, opting out is like turning down extra pay, denying yourself employer contributions which you will be able to access later in life.

A pension can be invested into a variety of alternative asset classes, which is where more complex self-invested pension options come in; self-invested personal pensions (SIPPs) and small self-administered schemes (SSASs) where you have the ability to invest in a wider pool of assets from an investment strategy point of view, meaning the pensions scheme is able to do the following:

- purchase and hold commercial property and

- loan to a connected company (SSAS only)

These types of planning are not right for everybody, and expert advice from a qualified financial adviser should be sought but, in certain circumstances, a pension can be a powerful tool to help build your business while accruing pension benefits that might not otherwise grow in the same way.

When you save into a pension, the government gives you tax relief as a way of rewarding you for saving for your future. When you make personal contributions to your pension, the money that you would have paid in tax on your earnings goes into your pension pot rather than to the government.

Tax relief is paid on your pension contributions at the highest rate of income tax you pay, so in the UK (except Scotland) it would be as follows:

- basic rate tax payer – 20% pension tax relief

- higher rate tax payer – 40% pension tax relief

- additional rate taxpayer – 45% pension tax relief

The rules in Scotland are different as income tax rates are different.

In real terms, this means that if you are a basic taxpayer, for every £80 you pay into your pension pot, you actually get £100 paid in. This is one of the benefits of a pension over a traditional savings account and is why pension savings are so important.

If your income is below the threshold at which you pay tax (currently £12,570 in 2021/22), you are eligible for a basic rate tax credit (20%) on personal contributions.

Even if you do not earn an income you can still contribute up to £2,880 per annum, which with tax relief claimed by the pension gives you a £3,600 gross contribution.

If you have built up your own pension pot in a defined contribution scheme, you can access the money in your pension pot from the age of 55 (rising to age 57 in 2028). Another advantage is that you can take up to a quarter (25%) of your pension savings as a tax-free lump sum.

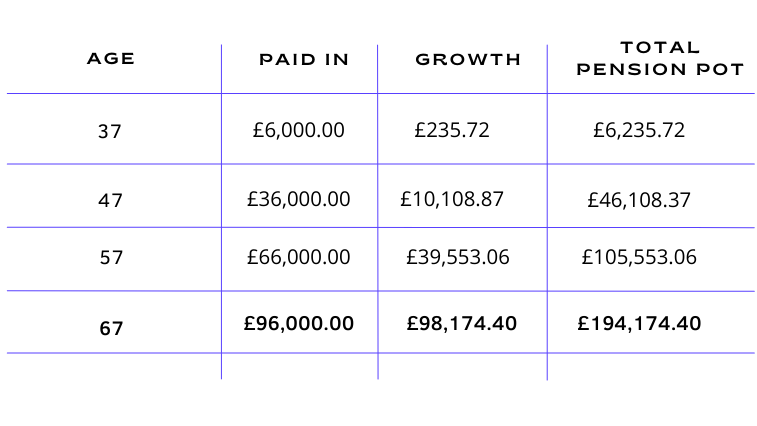

Case Study

Tom is aged 35 and has just started a job with a new employer, earning £30,000 per annum. He is paying 5% of his salary into his pension, which his employer is matching, giving a 10% pension contribution (£3,000 per annum). He has never paid into a pension before.

Assuming a conservative growth rate of 4% per annum, his pension could grow as follows:

As you can see, in the early years, growth is slower as the pot is smaller, but the closer he gets to his target retirement date of age 67, growth has compounded to such an extent that the growth on the investment is more than he has paid in.

Pensions are more complex than a bank savings account, but the tax benefits far outweigh those on offer and the investment options are greater. You cannot access your pension like you can with a savings account until you reach a certain age, which means it is there when you need it at retirement and worth more than if withdrawals could be made.

When making decisions, if you are unsure of the best course of action or if you would like advice on your pension and investment options, always seek expert professional help.

Sources:1 https://www.telegraph.co.uk/financial-services/pensions-advice-service/what-is-a-good-pension-pot/

Matthew O’Hara has worked in financial services since 2005, and loves working with people to help plan for their futures. Initially he worked in the banking sector, performing several different roles, working his way up to bank manager.

In 2018, he joined Mattioli Woods as a Wealth Management Consultant, continuing his passion for helping clients achieve their financial goals. He has extensive experience of working with individuals, business owners and professionals and provides holistic financial planning across all areas of wealth management.

Your article helped me a lot, is there any more related content? Thanks! https://accounts.binance.com/el/register-person?ref=B4EPR6J0

Your writing has a way of evoking strong emotions within me. I appreciate the way you elicit laughter, tears, and everything in between. Thank you for touching my heart.

Thanks for sharing. I read many of your blog posts, cool, your blog is very good. https://www.binance.info/ro/join?ref=S5H7X3LP